Budgeting with irregular income requires discipline, planning, and flexibility. According to the U.S. Bureau of Labor Statistics, about 16 percent of American workers are self employed or work in nontraditional arrangements, making irregular income a common challenge in today’s economy.

Why Irregular Income Requires Special Planning

Irregular income is common among freelancers, contractors, gig workers, and commission based employees. Unlike salaried workers who receive predictable paychecks, individuals with fluctuating earnings face unique challenges. Some months bring abundance, while others feel lean. Without a plan, these ups and downs can lead to stress and financial instability.

The challenge is not only financial but also psychological. When income is unpredictable, it is easy to feel anxious about whether you can cover rent or bills. A clear plan reduces that stress by showing exactly how much you need to save during strong months and how to adjust during lean ones. This approach transforms irregular income from a source of worry into a manageable system.

Budgeting with irregular income requires a mindset shift. Instead of focusing on what you earn in a single month, you must look at averages and long term patterns. By smoothing out the highs and lows, you create stability and reduce the risk of overspending.

Build a Buffer and Emergency Fund

One of the most important strategies for irregular income is creating financial cushions. A buffer fund smooths out monthly fluctuations, while an emergency fund protects against unexpected events. Saving during high income months ensures stability when earnings dip. This is where freelancer emergency fund planning becomes essential.

- Save extra income during strong months to cover lean periods.

- Aim for three to six months of expenses in a liquid emergency account.

A buffer fund is not the same as an emergency fund. The buffer is designed to handle predictable fluctuations, such as seasonal slowdowns or months when invoices are delayed. The emergency fund, on the other hand, is reserved for true surprises like medical bills or car repairs. Having both in place ensures you can continue meeting essentials without resorting to debt.

Building these funds requires discipline. It may mean setting aside more than you think you can spare during high earning months. However, the payoff is peace of mind. When lean months arrive, you will not scramble to cover rent or utilities. Instead, you can draw from reserves and stay on track.

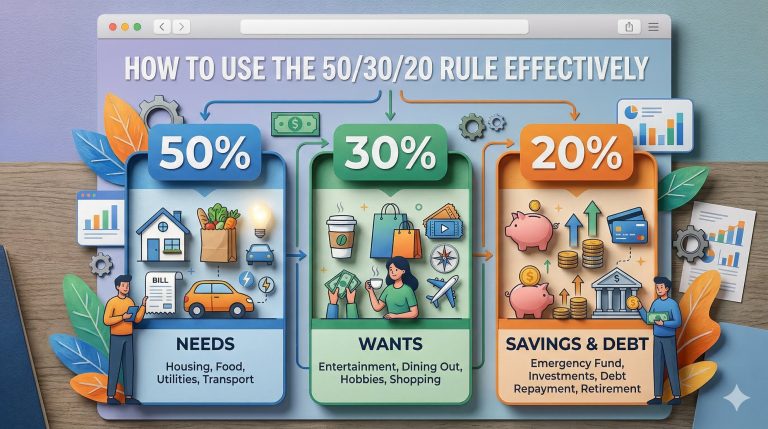

Use Percentage Based Budgeting

Traditional budgets assign fixed amounts, but irregular income benefits from percentages. This method adjusts spending based on actual earnings each month, keeping your plan flexible. Essentials, savings, and discretionary spending each receive a share of whatever comes in, so you never overcommit.

- Allocate percentages such as 50 percent for needs, 30 percent for wants, and 20 percent for savings.

- Adjust categories as income changes to maintain balance.

Percentage based budgeting is powerful because it scales with your income. If you earn more in a given month, your savings and discretionary categories grow proportionally. If you earn less, the system automatically reduces spending in non essential areas. This prevents overspending and ensures essentials are always prioritized.

Individuals who rely on freelance or gig work often find this approach especially useful. By agreeing with yourself on percentages, you create a consistent framework that adapts to whatever amount arrives. This transparency reduces stress and builds confidence in your financial plan.

Planning Beyond the Basics

Budgeting with irregular income is not just about numbers. It is about building habits that support long term stability. Tracking income and expenses regularly helps you spot patterns. For example, you may notice that certain months are consistently stronger, while others are weaker. Recognizing these cycles allows you to plan ahead.

Debt management is another critical area. High income months provide opportunities to pay down balances faster. Reducing debt during these times prevents interest from accumulating and frees up cash flow for essentials. Lean months then become less stressful because you are not burdened by large payments.

Taxes also require attention. Freelancers and contractors often face quarterly tax obligations. Setting aside a percentage of each paycheck for taxes prevents surprises. A separate account dedicated to tax savings ensures you are prepared when deadlines arrive.

Communication is equally important, even if you are budgeting alone. Being honest with yourself about spending habits and income expectations helps you stay disciplined. Regular self check ins allow you to adjust when circumstances change.

Budgeting with irregular income teaches discipline and resilience. It forces you to plan ahead, save consistently, and adapt quickly. Over time, these habits strengthen financial health and reduce stress. Individuals who master budgeting gain confidence and stability, even in unpredictable markets.

The benefits extend beyond finances. Knowing you have a plan reduces anxiety and allows you to focus on work. Instead of worrying about whether you can pay bills, you can concentrate on growing your business or career. This mental clarity is one of the most valuable outcomes of effective budgeting.

Irregular income presents unique challenges, but with planning and discipline, it is manageable. With patience and consistency, budgeting with irregular income becomes a path to financial security rather than stress.